If you own a business, general liability insurance isn’t optional — it’s foundational. Yet one of the most searched questions on Google is:

“What is included in a general liability policy?”

Let’s break it down clearly so you know what you’re actually buying.

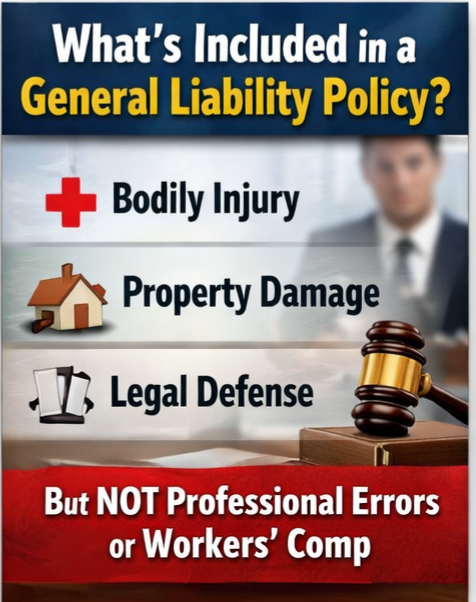

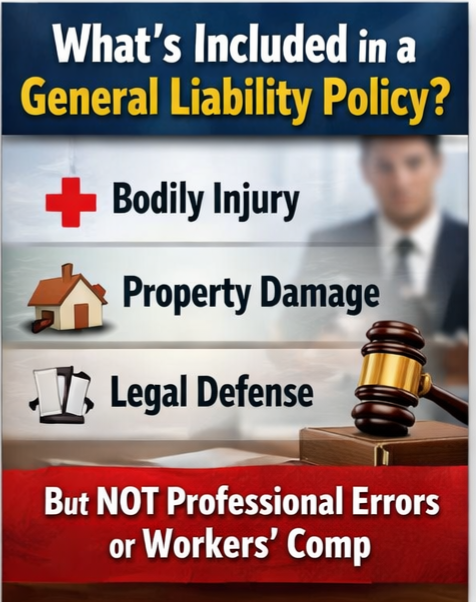

What General Liability Insurance Typically Covers

A general liability (GL) policy is designed to protect your business from third-party claims involving bodily injury, property damage, and certain legal issues.

1. Bodily Injury

If someone is injured because of your business operations, your policy can help cover:

- Medical bills

- Legal defense costs

- Settlements or judgments

Example: A client slips on a wet floor in your office.

2. Property Damage

If you or your employees damage someone else’s property, this coverage can respond.

Example: You’re installing equipment at a customer’s location and accidentally damage their flooring.

3. Personal & Advertising Injury

This includes:

- Libel or slander

- Copyright infringement

- Advertising mistakes

If someone claims your marketing caused financial harm, this portion may apply.

4. Legal Defense Costs

Even if a claim is groundless, your policy typically covers attorney fees and court costs. And legal defense alone can cost thousands — fast.

What General Liability Does NOT Cover

Here’s where many business owners get caught off guard.

General liability does not cover:

- Professional mistakes (that’s professional liability)

- Employee injuries (that’s workers’ comp)

- Auto accidents (that’s commercial auto)

- Data breaches (that’s cyber liability)

- Damage to your own property (that’s property insurance)

This is why most businesses need a combination of coverages — not just one policy.

Why It Matters

Many contracts require general liability before you can:

- Lease space

- Work with larger clients

- Bid on jobs

- Join vendor networks

But more importantly, one claim could financially cripple a small business without coverage.

If you’re not sure whether your current policy actually protects you the way you think it does, that’s worth reviewing. CONTACT US