Let’s be honest—insurance terms can feel like a different language.

Deductibles. Limits. Premiums.

You’ve probably seen these words on your policy… but no one has ever really sat down and explained them in a way that actually makes sense.

So let’s fix that. No jargon. No fluff. Just a real conversation.

First—The Big Picture

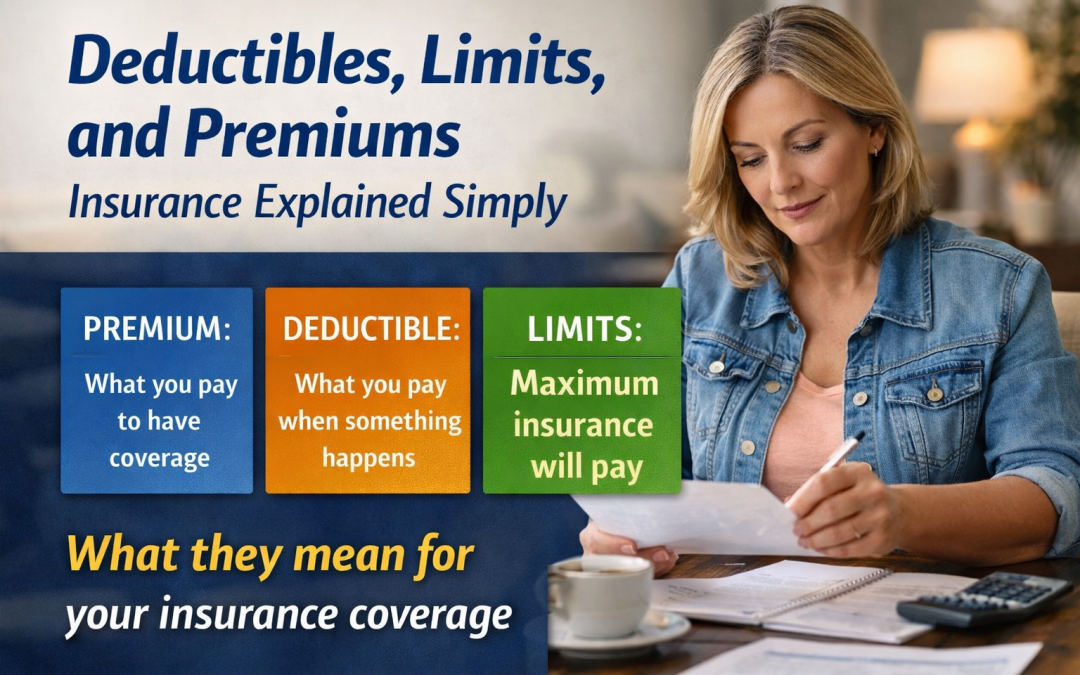

Every insurance policy comes down to three things:

- What you pay every month (premium)

- What you pay when something happens (deductible)

- How much protection you actually have (limits)

Once you understand these three, everything else starts to click.

1. Premium: What You Pay to Have the Coverage

Your premium is your monthly (or annual) payment to keep your insurance active.

Think of it like a membership:

You’re paying for protection—even if you never use it.

👉 Example:

- Your home insurance costs $2,000 per year

- That’s your premium

Here’s the part people don’t love hearing:

Lower premium usually means less coverage or more risk on your end.

If someone tells you they “got a better deal,” it’s worth asking:

Did they actually get better coverage… or just cheaper coverage?

2. Deductible: Your Share When Something Goes Wrong

Your deductible is what you pay out of pocket before insurance kicks in.

Think of it like this:

You and the insurance company are sharing the cost—but you go first.

👉 Example:

- You have a $2,500 deductible on your home policy

- A storm causes $10,000 in damage

- You pay $2,500

- Insurance pays the remaining $7,500

Simple enough, right?

Now here’s where people get tripped up:

👉 Higher deductible = lower premium

👉 Lower deductible = higher premium

So it’s a trade-off.

The real question is:

If something happened tomorrow, could you comfortably afford your deductible?

Because if the answer is no, that “cheap” policy isn’t really doing you any favors.

3. Limits: Your Financial Protection Ceiling

Your limits are the maximum amount your insurance will pay.

This is where real protection lives—and where most people are underinsured.

👉 Example:

- Your liability limit is $300,000

- You’re involved in a serious accident and are sued for $600,000

You’re responsible for the remaining $300,000.

That’s not a small gap—that’s life-changing.

Where Limits Matter Most:

- Liability (home + auto) → protects your assets and future income

- Dwelling coverage → cost to rebuild your home

- Personal property → everything inside your home

👉 If your limits are too low, your policy can run out before the problem is solved.

How These Three Work Together

Here’s the simplest way to think about it:

- Premium = what it costs to have protection

- Deductible = your upfront responsibility

- Limits = how much protection you actually have

And here’s the truth most people miss:

👉 You can’t just focus on one.

A low premium with a high deductible and low limits might look good…

until you actually need it.

The Most Common Mistake

Most people shop insurance based on price alone.

But what they’re really doing is unknowingly adjusting:

- Their deductible (higher than they can afford)

- Their limits (lower than they need)

And they don’t realize it until it’s too late.

A Better Way to Think About It

Instead of asking:

“How can I get this cheaper?”

Ask:

“If something happens, will this actually protect me?”

That one shift changes everything.

Final Thought

You don’t need to memorize insurance terms.

You just need to understand how they affect your real life.

Because at the end of the day, insurance isn’t about policies—

it’s about what happens when something goes wrong.

And that’s not the time you want surprises. Contact Us for a Quote