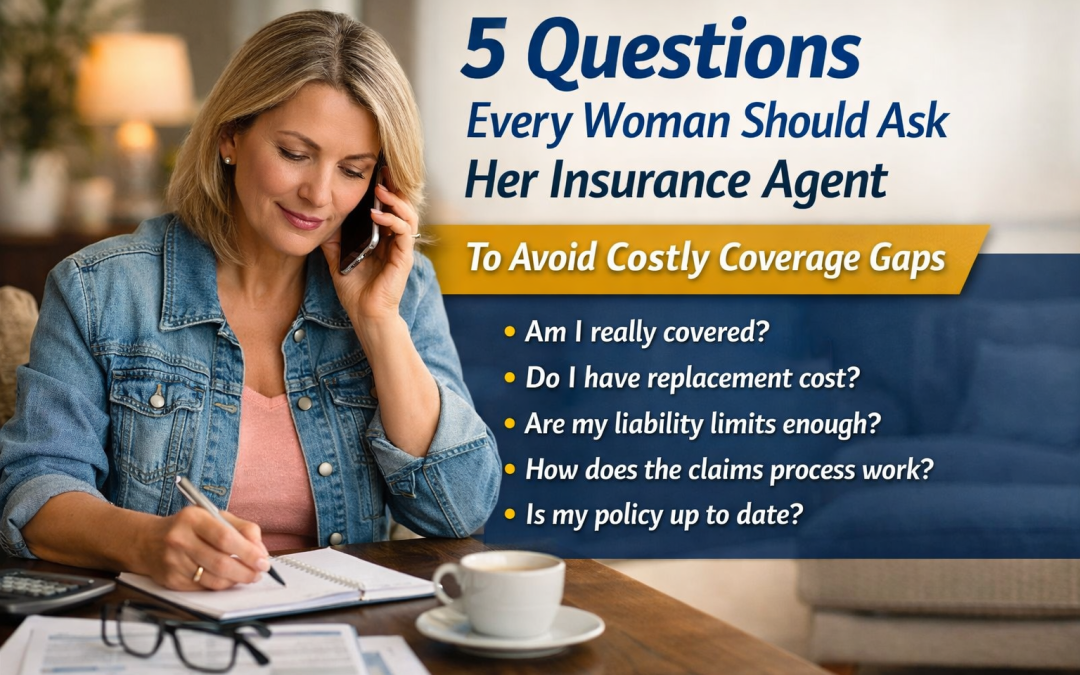

Insurance shouldn’t feel confusing or overwhelming—but for a lot of women, it does. You’re managing a household, protecting your family, and making smart financial decisions… yet most policies are written in a way that makes it hard to know if you’re actually covered.

Here’s the truth:

If you don’t ask the right questions, you can end up with coverage that looks good on paper—but fails you when you need it most.

Let’s fix that.

1. “What am I not covered for?”

This is the question almost no one asks—and it’s the one that matters most.

Most people assume their policy covers “everything.” It doesn’t.

Common gaps include:

- Water damage (depending on the source)

- Foundation issues

- Certain roof claims

- Liability situations that exceed your limits

👉 A good agent should clearly explain your exclusions—not dance around them.

Why it matters:

Claims get denied in the gaps. If you don’t know where those gaps are, you’re taking a risk whether you realize it or not.

2. “Do I have replacement cost or actual cash value?”

This one can cost you thousands if you get it wrong.

- Replacement Cost = pays to replace your items at today’s prices

- Actual Cash Value (ACV) = pays what your items are worth after depreciation

That roof, couch, or flooring? If it’s older and you have ACV, you may only get a fraction of what it costs to replace.

👉 And here’s what most people don’t realize:

Many policies automatically shift parts of your coverage (like roofs) to ACV over time.

Why it matters:

You don’t want to find out after a loss that you’re only getting half of what you expected. Learn More

3. “Are my liability limits high enough to protect me?”

This is where real financial protection happens—and where most people are underinsured.

If someone is injured in your home, your dog bites someone, or you’re at fault in a serious auto accident… you could be sued.

Minimum limits are often not enough.

👉 Ask your agent:

- What would happen if I were sued?

- How much protection do I actually have?

- Should I consider an umbrella policy?

Why it matters:

Your home, savings, and future income could all be at risk without proper liability coverage.

4. “If I had to file a claim tomorrow, what would it look like?”

Most people don’t think about the claims process until they’re in the middle of it—and stressed.

Ask:

- What’s my deductible?

- How does the process actually work?

- What do I need to document?

- Should I call you before filing?

👉 A strong agent will walk you through this step-by-step. When to file a claim

Why it matters:

Knowing what to expect ahead of time helps you make better decisions—and avoid costly mistakes (like filing small claims that shouldn’t be filed).

5. “When was the last time my coverage was reviewed?”

Life changes. Your insurance should too.

Think about what’s changed in the last few years:

- Home value increases

- Renovations or upgrades

- Teen drivers

- New assets or savings

- Changes in marital status

If your policy hasn’t been reviewed recently, there’s a good chance it’s outdated.

👉 A proper review should happen at least once a year.

Why it matters:

Outdated coverage is one of the biggest reasons people find themselves underinsured.

The Bottom Line

Insurance isn’t just about having a policy—it’s about having the right protection in place for your life today.

The women who feel the most confident about their coverage aren’t the ones who bought the cheapest policy…

They’re the ones who asked better questions.

Final Thought

You don’t need to become an insurance expert.

You just need an agent who’s willing to slow down, explain things clearly, and help you make smart decisions.

And if your current agent isn’t doing that?

That’s your answer right there. Contact Us