When it comes to homeowners insurance, one of the most misunderstood—and most costly—details is how your policy pays out after a loss. The difference between Actual Cash Value (ACV) and Replacement Cost (RC) can mean thousands of dollars out of your pocket if you’re not careful.

Let’s break it down in plain terms so you know exactly what you’re getting.

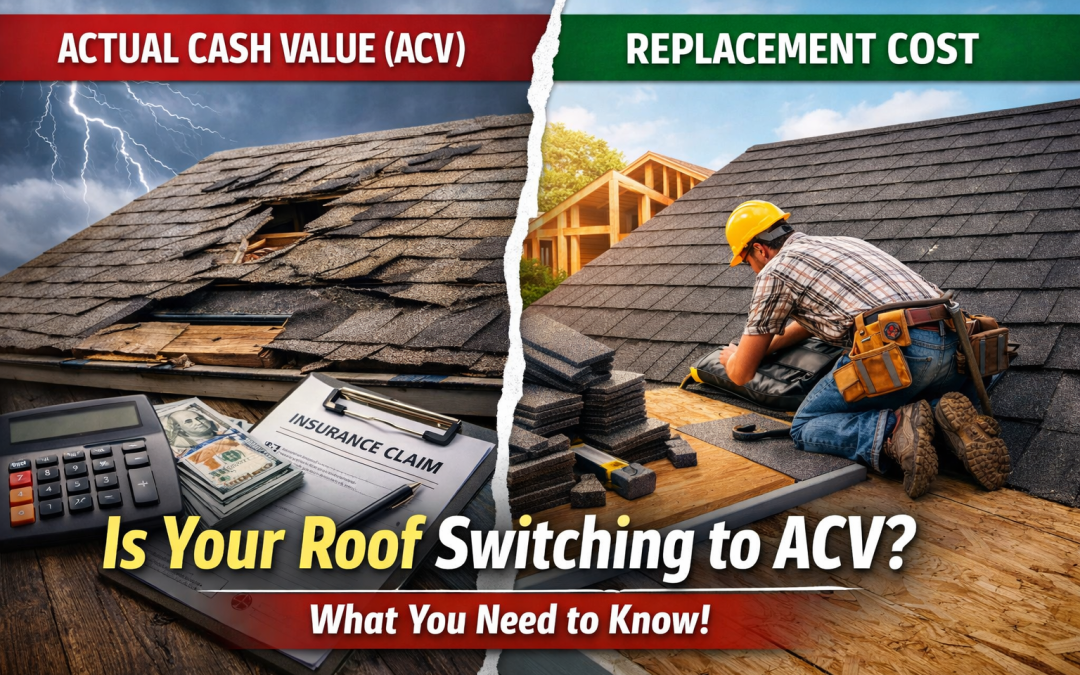

What Is Actual Cash Value (ACV)?

Actual Cash Value is what your property is worth today after depreciation.

Insurance companies look at:

- Age

- Wear and tear

- Condition at the time of loss

Then they reduce your payout accordingly.

Example:

You have a 10–15-year-old roof. A new roof costs $20,000 today. Because your roof isn’t new, the insurance company may only value it at $7,000–$10,000.

That’s your check (minus your deductible).

👉 The rest? That’s on you.

What Is Replacement Cost (RC)?

Replacement Cost is exactly what it sounds like:

the amount it takes to replace or rebuild with new materials at today’s prices.

No depreciation. No penalty for age.

Example:

Same roof. Same $20,000 replacement.

With replacement cost coverage, your policy pays what it actually costs to replace it (minus your deductible), so you can restore your home properly.

The Real-World Difference

Here’s where this really hits home:

| Scenario | ACV Payout | Replacement Cost Payout |

|---|---|---|

| Roof Replacement | Partial (depreciated) | Full cost to replace |

| Furniture Loss | Used value | New replacement |

| Flooring Damage | Aged value | New materials |

ACV leaves gaps. Replacement Cost closes them.

⚠️ The Shift Most Homeowners Don’t See Coming: Roofs Eventually Go ACV

Here’s the part the industry doesn’t always explain clearly:

At some point, most insurance companies will stop offering replacement cost on your roof if it hasn’t been replaced.

Instead, they switch your roof coverage to Actual Cash Value.

Why?

- Older roofs are more likely to fail

- Claims are more frequent and more expensive

- Insurers limit their risk by depreciating payouts

👉 In many cases, once a roof hits a certain age (often around 8-10+ years depending on the carrier and roof type), you’ll see:

- A policy endorsement changing roof coverage to ACV

- A renewal notice with reduced coverage

- Or higher premiums unless you replace the roof

What That Means for You

Let’s be real—this is where homeowners get hit the hardest.

If your older roof is covered on ACV and gets damaged:

- The insurance company will not pay for a full replacement

- You may receive only a fraction of the cost

- You’ll likely have to come out of pocket for the majority of the new roof

Example:

A 17-year-old roof is damaged in a storm. Replacement cost is $20,000.

ACV payout might be $5,000–$8,000.

That gap doesn’t go away—you pay it.

Where Homeowners Get Caught Off Guard

This is the part most people don’t realize:

👉 Your policy may not be all one or the other.

Many homeowners policies are structured like this:

- Dwelling (your home): Replacement Cost

- Roof (older): Actual Cash Value ❌

- Personal Property (your stuff): Actual Cash Value ❌ (unless upgraded)

So even if you think you have “great coverage,” parts of your home—and everything inside it—may still be depreciated.

That’s where claims start to feel disappointing.

Why This Matters More Than Ever

Costs to rebuild homes have increased significantly in recent years. Labor, materials, and supply chain issues all drive prices up.

If your coverage is based on depreciated values, you may find yourself:

- Unable to fully repair damage

- Paying large out-of-pocket costs

- Forced to delay or patch repairs instead of replacing

And when it comes to roofs, waiting too long can cost you twice—once in reduced coverage, and again in higher premiums.

The Bottom Line

If you want your home and your life put back together the way it was before a loss, replacement cost coverage is the better option—period.

But here’s the bigger takeaway:

👉 Replacement cost on a roof isn’t guaranteed forever.

At some point, if the roof isn’t replaced, your policy will likely shift to ACV—and that changes everything.

Final Thought

Insurance shouldn’t leave you halfway covered—but it often does if you’re not paying attention.

If you’re not sure:

- How your roof is covered

- Whether your policy has already switched to ACV

- Or when that change might happen

It’s time to review it.

Because the worst time to find out you have ACV coverage… is after the damage is done.

If you’d like help reviewing your policy and making sure there are no surprises, I’m happy to walk through it with you. Contact us